The Hard Drive Boom’s Rare-Earth Reckoning Arrives by 2031

Table Of Contents

show

The technology industry is in the middle of a hard drive shortage unlike anything it has seen in years. Artificial intelligence data centers are buying storage faster than manufacturers can build it, and nearly all of the attention is on what is going in: sold-out capacity, orders locked years ahead, and steadily rising prices. Far less attention is being paid to the other end of the story. Every one of those drives has a service life measured in just a few years. When that life ends, the drive becomes something else entirely — part of a growing stream of retired hardware carrying metals that have quietly turned strategically valuable. This is a look at where that stream is heading, why the materials inside a spinning disk suddenly matter, and what the next several years of hard drive recycling are likely to look like as the wave crests around 2031.

The demand wave everyone is watching

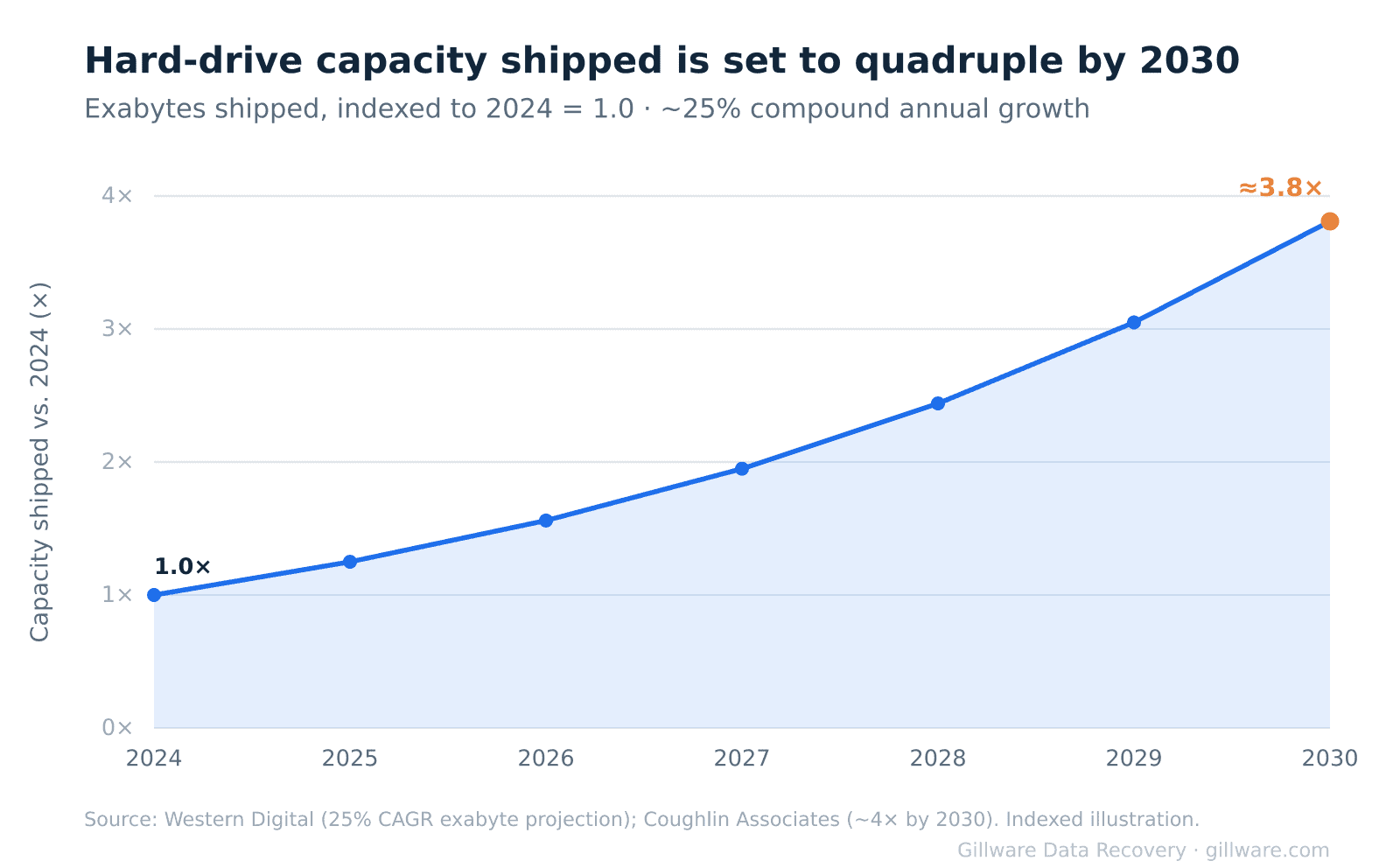

The scale of the current buildout is hard to overstate. Western Digital has projected hard drive capacity demand growing at roughly 25% per year — above its earlier estimates — driven largely by AI workloads that generate and retain enormous volumes of data. Independent analysts at Coughlin Associates extrapolate that hard drive capacity shipments in 2030 will run about four times higher than in 2024. Storage, unlike compute hardware, is cumulative: an AI system keeps producing data that has to live somewhere long after the servers that made it are retired.

That demand has collided with a supply base that cannot expand quickly. Hard drive production depends on specialized components — precision read/write heads and media — that cannot be ramped the way flash memory can with new fabrication lines. The result is a market that tightened fast: manufacturers have reported nearline capacity fully allocated well into the near future, with cloud customers locking in orders extending toward the end of the decade. Nearly nine-tenths of major manufacturers’ hard drive revenue now comes from cloud and enterprise buyers. Meanwhile the number of hyperscale data centers, already past 1,100 at the end of 2024, is projected to roughly triple by 2030. The front end of this story is a boom. The back end is what almost no one is planning for.

Every drive comes back: the retirement wave

Data centers do not keep hard drives forever. In a high-utilization environment, drives are typically cycled out every two to three years — sometimes stretched further, but rarely by much, because reliability and warranty economics favor replacement over risk. That short life is the key to the whole story. A drive purchased during the 2025–2028 surge does not disappear once it is installed. It comes back out, on schedule, a few years later.

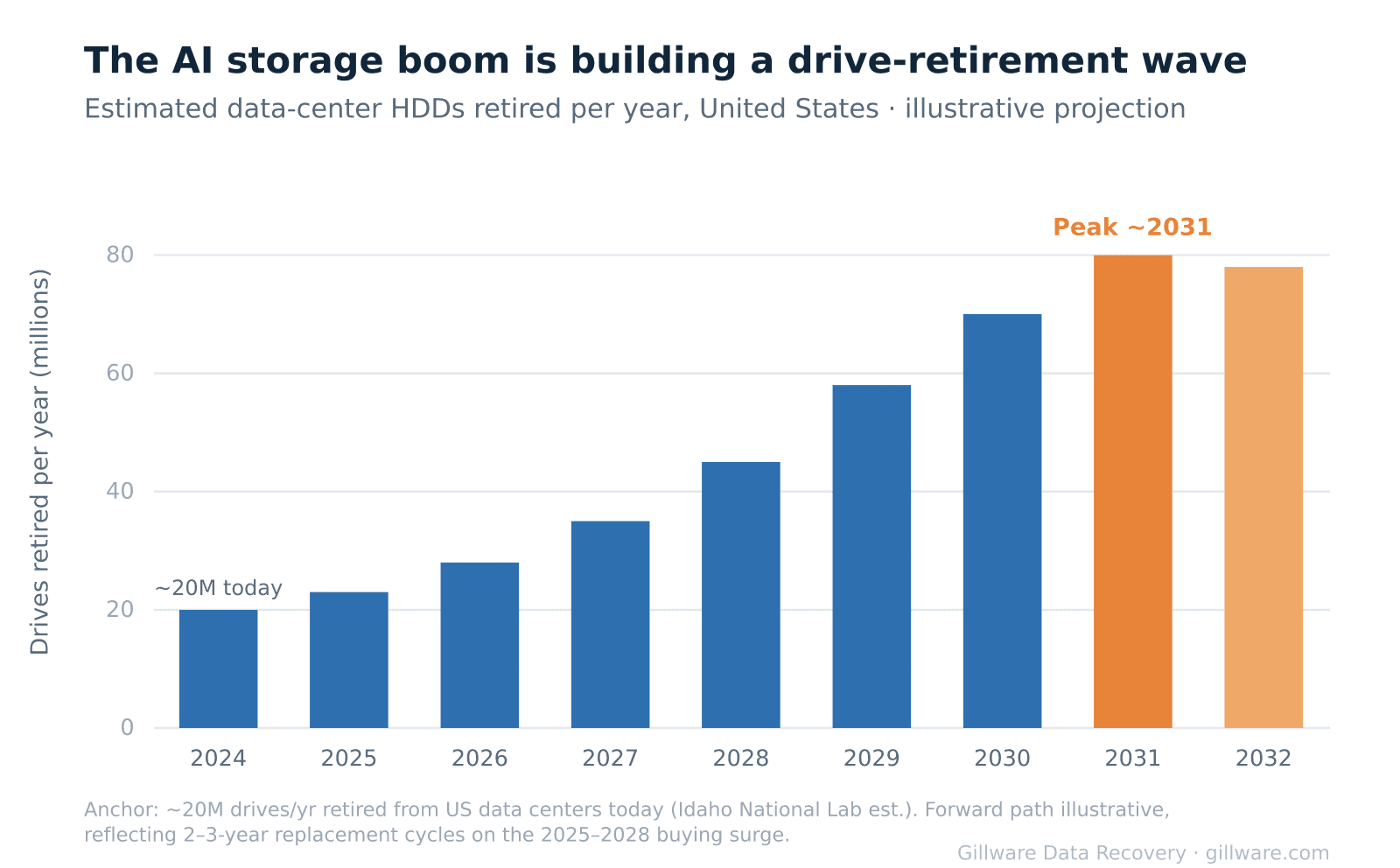

Run that math forward and the shape of the next decade becomes clear. The record volumes going into data centers today become a record volume of retired drives roughly three years later — a decommissioning wave that builds through the late 2020s and concentrates around 2031. Researchers at Idaho National Laboratory have estimated that something on the order of 20 million hard drives are already retired from major U.S. data centers every year. As the AI buildout ages out, that number climbs steeply.

This lands on a recycling system that is not ready for it. The United States generates roughly 8 million tons of electronic waste a year, and only an estimated 15 to 20 percent of it is properly recycled. Hard drives are a small slice of that total by weight, but a disproportionately important one by content — and the way they are currently handled at end of life leaves most of their value on the table.

What is inside — and why it suddenly matters

Strip a 3.5-inch hard drive down to its parts and the material breakdown is unremarkable at first glance. Roughly 60 percent of the weight is the aluminum casing and chassis. There is steel in the structure, copper in the voice coil that moves the read/write heads, and a small amount of gold and other precious metals plated onto the controller board — typically only a dollar or two worth per drive, and recoverable only through chemical refining, not a garage torch.

The valuable part is smaller and easy to miss: the rare-earth magnet that positions the drive’s heads with extraordinary precision. That magnet is built from neodymium, praseodymium, and often dysprosium — the same elements that go into electric-vehicle motors and wind turbines, and the same elements now at the center of a global supply-chain contest. This is why the arithmetic of the retirement wave changes everything. A single dead drive is worth pennies as scrap. Twenty, forty, eighty million of them a year is a rare-earth resource. At Gillware, we have spent more than two decades opening these devices at the component level, and the irony is not lost on us: the part that fails least often is the part the world now most wants back.

The rare-earth reckoning

Why the metals used to vanish

For most of the hard drive era, the rare earths inside retired drives simply disappeared. Conventional recycling melted the drives down with the steel stream, where the rare-earth content was contaminated and effectively lost. Recovering it separately was corrosive, complex, and rarely worth the cost when the metals were cheap and plentiful. The result: the U.S. recycling rate for rare-earth elements has historically sat below 10 percent. The materials were mined once, used once, and thrown away.

The acid-free breakthrough

That is beginning to change, and quickly. In a pilot completed at the end of 2024, Western Digital worked with Microsoft and the recyclers CMR and PedalPoint to process close to 50,000 pounds of shredded end-of-life drives and related equipment. Using an acid-free process, the effort recovered rare-earth elements — including neodymium, praseodymium, and dysprosium — alongside gold, copper, and other metals, at rates reported around 90 percent for the rare earths. Just as significant as the yield was the footprint: recovering the material this way was estimated to cut greenhouse-gas emissions by roughly 95 percent compared with mining and refining it from scratch.

The importance of that pilot is not the single batch. It is the proof that a domestic, non-toxic recovery process can work at industrial scale on exactly the material the retirement wave is about to produce in enormous quantity.

Beyond a single pilot

The movement is broader than one partnership. Apple has worked with domestic rare-earth producer MP Materials to build recycled magnet material into its supply chain. Google has run experiments reusing hard drive magnets rather than shredding them. Researchers at Oak Ridge National Laboratory have demonstrated an automated line capable of processing thousands of drives a day to pull magnets out intact. And the hyperscaler recovery programs that produced the 2024 pilot are being extended to additional partners. None of this is yet operating at the scale the retirement wave will demand — but the direction is unmistakable. Recovery is shifting from a research curiosity to an emerging industry, and it is doing so just ahead of the volume that will justify it.

The security paradox

There is a genuine tension standing in the way, and it is worth being honest about. The dominant end-of-life practice for data-center drives is physical destruction — shredding — driven by legitimate data-security and compliance obligations. When a drive has held sensitive records, the safest assumption is that the data cannot be allowed to survive, and shredding delivers that certainty in a way an organization can document for auditors and regulators.

The problem is that shredding is precisely what turns a recoverable rare-earth magnet into unrecoverable dust. The same act that guarantees the data is gone also destroys the most valuable material in the device. This has opened a real debate across the IT asset disposition world between shredding everything by default and a more selective approach: securely erasing drives so they can be reused or their components recovered whole. Reuse carries its own math — extending a drive’s life prevents several times more carbon emissions than shredding and recycling it does. There is no simple answer here, because the security requirement is real. But as the retirement volume grows, the cost of defaulting to the shredder — measured in strategic metals reduced to powder — grows with it.

The price signal and the clean-loop divide

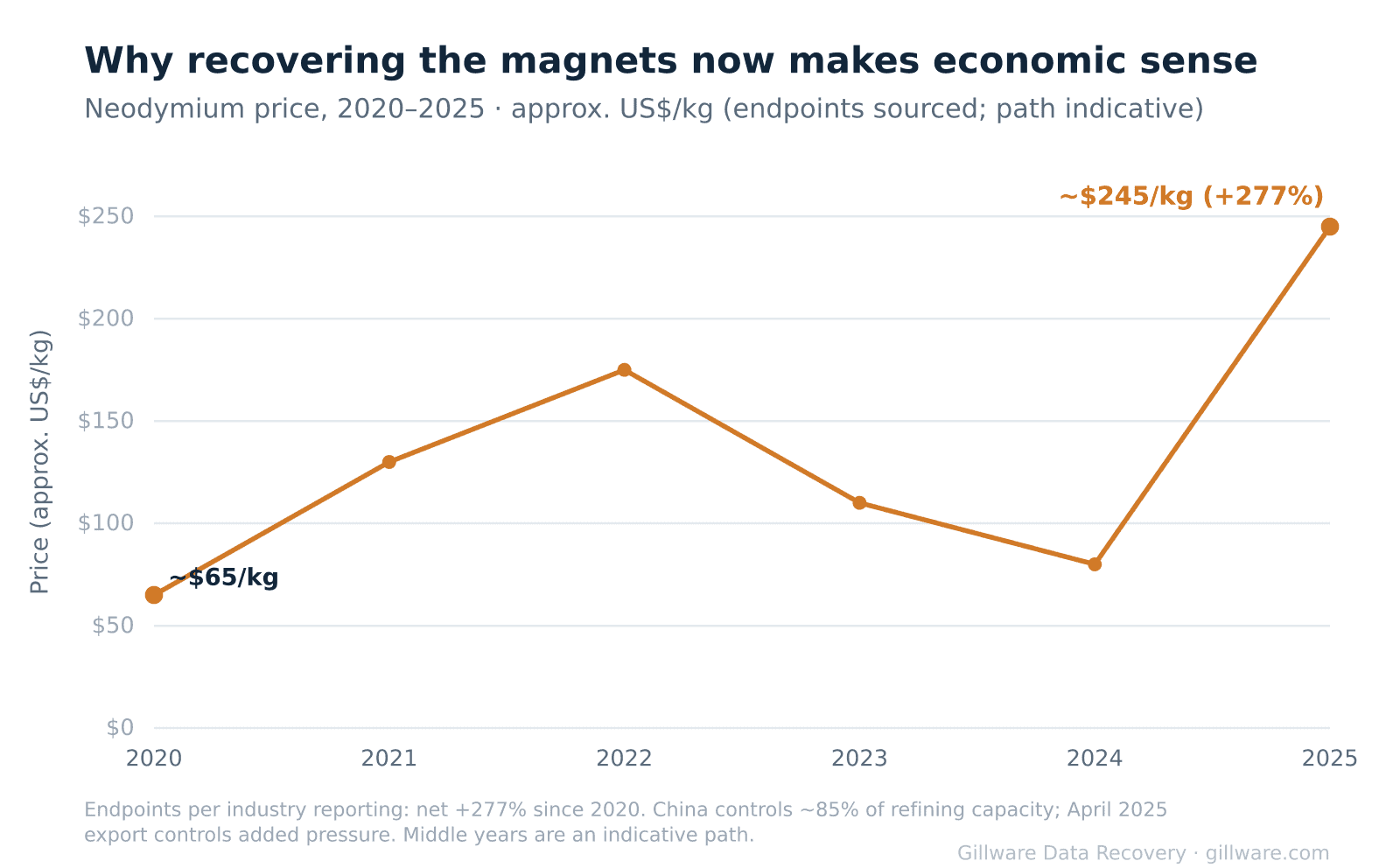

Economics are what ultimately move a practice from wasteful to worthwhile, and the economics have shifted hard. Neodymium prices have risen roughly 277 percent since 2020. The supply picture explains much of the pressure: a single country controls an estimated 85 percent of global rare-earth refining capacity, and in April 2025 it imposed export licensing requirements on several rare-earth elements, including neodymium, praseodymium, and dysprosium. When the material becomes both expensive and uncertain to source, recovering it from drives you already own stops looking like environmental goodwill and starts looking like supply-chain insurance.

There is also a sharp contrast in how this material gets recovered around the world. As of the start of 2025, international rules under the Basel Convention tightened restrictions on cross-border shipments of electronic waste — an agreement the United States, notably, has not joined. In parts of the world, electronic waste is still processed informally, using open burning and acid leaching to strip out gold and copper. Those methods are cheap, but they have made a handful of processing sites among the most polluted places on earth and exposed the people working them to serious harm. The domestic recovery approach now being piloted — acid-free, contained, and closed-loop — is the deliberate opposite of that. The same chemistry that is a public-health disaster in an open pit can, engineered properly, become a clean industrial process. Which path a given ton of retired drives follows is, increasingly, a policy and infrastructure choice rather than a technical one.

What the next few years look like

Put the pieces together and the shape of the late 2020s comes into focus. A retirement wave of unprecedented size is building toward roughly 2031. The metals inside those drives have become strategically valuable and politically contested. And a domestic recovery industry is emerging — proven in pilots, not yet built to scale — right as the raw material begins to arrive. The open question is timing. If recovery capacity grows fast enough to meet the wave, retired hard drives become a meaningful domestic source of critical materials and a genuine circular-economy success story. If it does not, tens of millions of drives a year will keep flowing to shredders and smelters, and the rare earths inside them will be lost again — mined once, used once, and thrown away, at exactly the moment the world can least afford it.

For anyone who manages storage at scale, the practical takeaway is that end-of-life is becoming a decision worth making deliberately rather than by default. How drives are retired, whether they are erased or destroyed, and where they go afterward are questions with real financial, environmental, and security weight attached — and they are only going to get heavier as 2031 approaches.

Gillware has spent more than two decades working inside these devices — recovering data from the same hard drives, arrays, and storage systems now moving through their end-of-life. It is a vantage point that makes the coming recycling wave less an abstraction than a familiar object seen from a new angle.