How a Hard Drive Is Made in 2026: The Global Supply Chain, Mapped

Table Of Contents

show

In early 2026, something happened to the humble hard drive that almost nobody outside the storage industry saw coming: the world ran out of them. Western Digital and Seagate — two of the three companies left that still make hard disk drives — told investors that essentially their entire 2026 production of high-capacity “nearline” drives was already spoken for, sold in advance to the hyperscale data centers building out artificial intelligence. Street prices for ordinary drives climbed by roughly half in a matter of months, and lead times for enterprise drives stretched toward two years.

How does a device that has been mass-produced by the hundreds of millions for four decades suddenly become scarce? The short answer is a demand shock. The longer, more interesting answer is that a modern hard drive is one of the most globally distributed objects you will ever hold — a palm-sized assembly of rare-earth magnets, ultra-smooth glass, nanometer-scale magnetic heads, custom silicon, and precision motors, drawn from a supply chain that spans a dozen countries and a handful of effectively irreplaceable suppliers. Pull on any one thread and the whole thing can seize up.

This is a map of that supply chain as it stands in 2026. We’ll open up a drive, trace every major component back to where its materials are mined and where its parts are made, look at what happened the last time the chain broke, and weigh where it might be vulnerable next. It’s a story that runs from mines in a handful of countries, through cleanrooms in Japan and Ireland, to assembly lines in Southeast Asia, and finally into the server racks that increasingly define the digital economy.

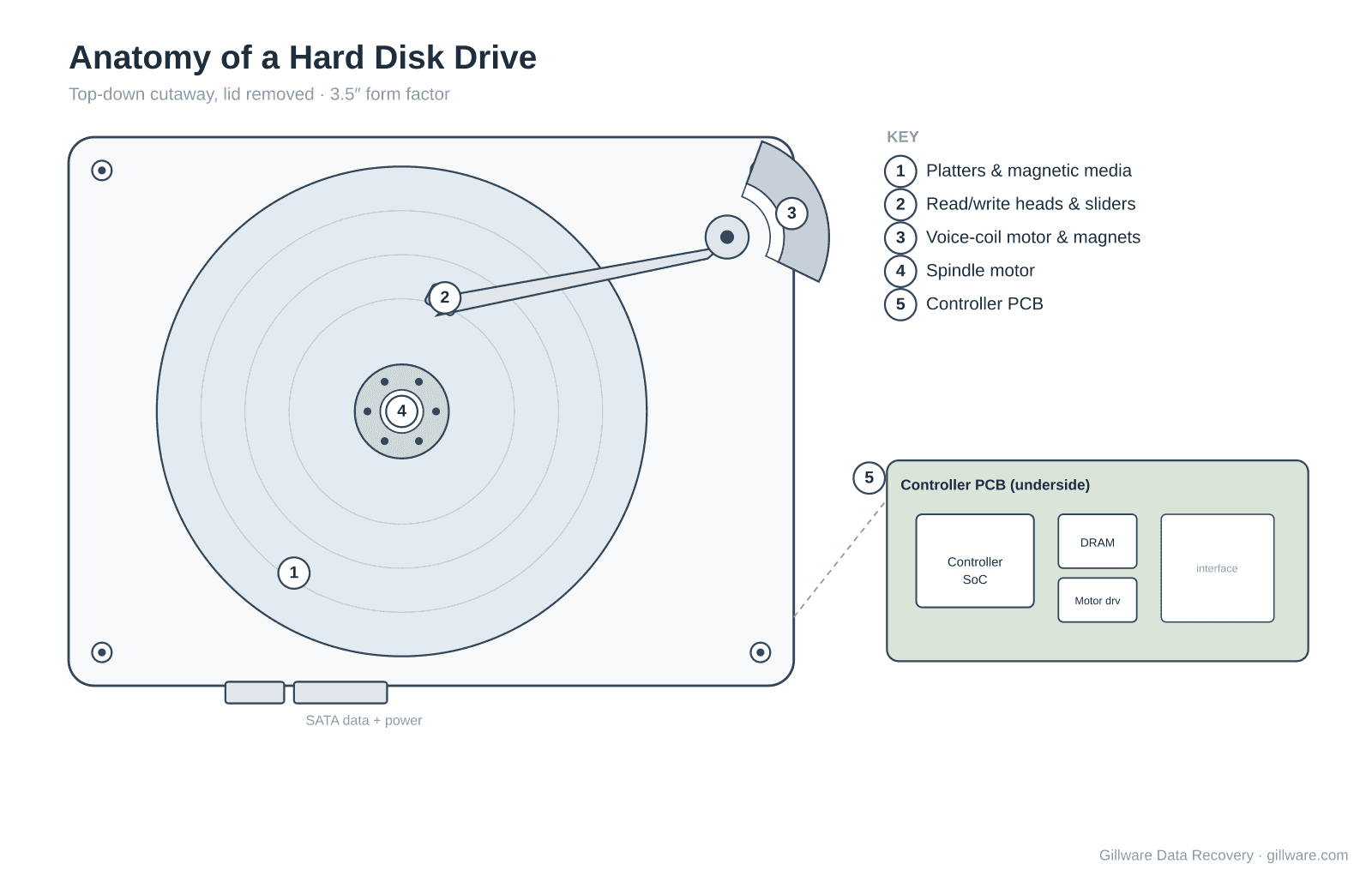

Anatomy of a modern hard drive

Before we trace the parts around the world, it helps to know what they are. Strip the lid off a 3.5-inch enterprise hard drive and you’ll find a remarkably consistent set of components, refined but not fundamentally reinvented since the 1990s.

The heart of the drive is a stack of platters — rigid, mirror-smooth disks that spin thousands of times a minute and hold the data itself in a microscopically thin magnetic coating. Floating just above each platter surface, at a gap of a few nanometers, is a read/write head mounted on a small ceramic block called a slider. The heads ride on the ends of actuator arms, swung across the disk by a voice-coil motor whose muscle comes from a pair of powerful permanent magnets. Underneath everything, a spindle motor turns the platters, and a controller board bolted to the outside of the sealed enclosure runs the firmware, manages the heads, and talks to the host computer. Many high-capacity drives are also sealed and filled with helium, which is thinner than air and lets platters spin with less turbulence.

Every one of those components is a specialty product in its own right, and for several of them the entire world depends on a very small number of suppliers. That concentration is the theme of everything that follows.

One more feature of high-capacity modern drives is worth flagging, because it drives so much of the 2026 story: the relentless race to fit more terabytes into the same 3.5-inch box. Manufacturers have pushed capacity up by sealing drives and filling them with helium — which is about one-seventh the density of air, so platters spin with far less drag and turbulence, allowing more, thinner platters to be packed in and the heads to fly more stably. On top of that, density technologies such as Heat-Assisted Magnetic Recording (HAMR) are pushing individual drives toward and beyond the 30-terabyte mark, with roadmaps pointing to 100 terabytes later this decade. This is the industry’s main answer to surging demand: rather than build many more factories, make each drive hold far more. It is an elegant solution, but it also means the newest, highest-value drives depend on the most advanced — and most concentrated — media, heads, and manufacturing processes in the whole chain.

How the world came down to three drive makers

The concentration we’re about to trace didn’t happen by accident — it is the result of two decades of consolidation. In the 1990s and early 2000s there were roughly ten companies making hard drives, names like IBM, Fujitsu, Maxtor, Quantum, Samsung, Hitachi, Seagate, Toshiba, and Western Digital. Making hard drives is a brutally capital-intensive business: each new generation demands enormous investment in cleanrooms, head fabs, and media lines, and margins are thin. Over time, the companies that couldn’t sustain that spending were acquired or exited.

The endgame arrived around 2011 and 2012 — the same window as the Thailand floods discussed below. Western Digital acquired Hitachi’s hard-drive division (the former IBM storage business), and Seagate acquired Samsung’s hard-drive operations, while Toshiba had earlier absorbed Fujitsu’s drive business and later picked up assets divested to satisfy regulators reviewing the other two deals. When the dust settled, three companies remained: Seagate, Western Digital, and Toshiba. That is still the entire field in 2026.

This matters for the supply-chain story in two ways. First, three makers means three sets of purchasing decisions determine demand for every upstream component — heads, media, motors, magnets, silicon — which is part of why those supplier bases are themselves so concentrated. Second, with no new entrants and enormous barriers to building fresh capacity, the industry’s response to a demand surge is necessarily slow. You cannot simply spin up a new hard-drive company to meet a shortage; the expertise, the equipment, and the supplier relationships took decades to build. When we say the chain has little slack, this is a large part of why.

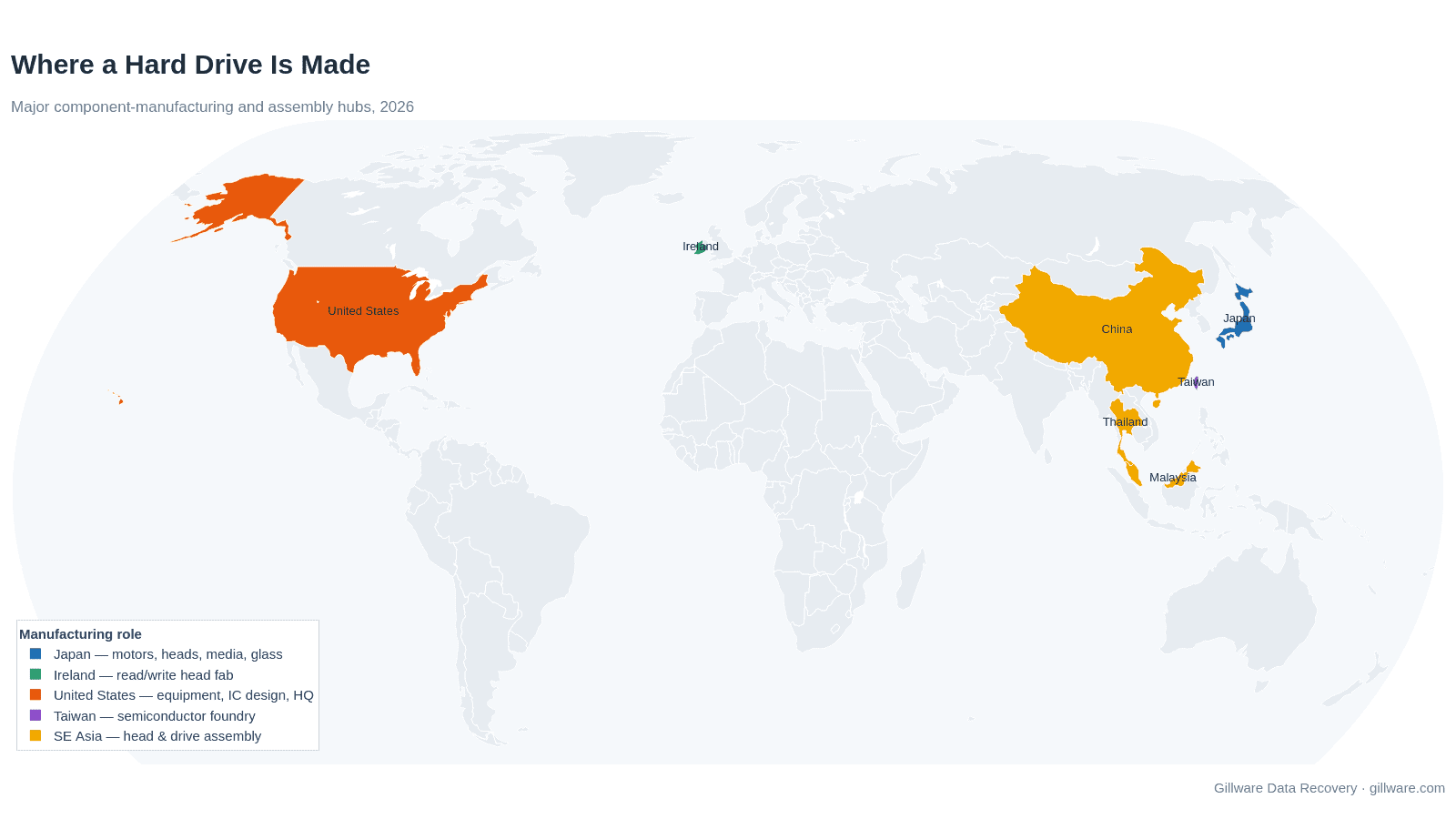

The world tour: where a hard drive actually comes from

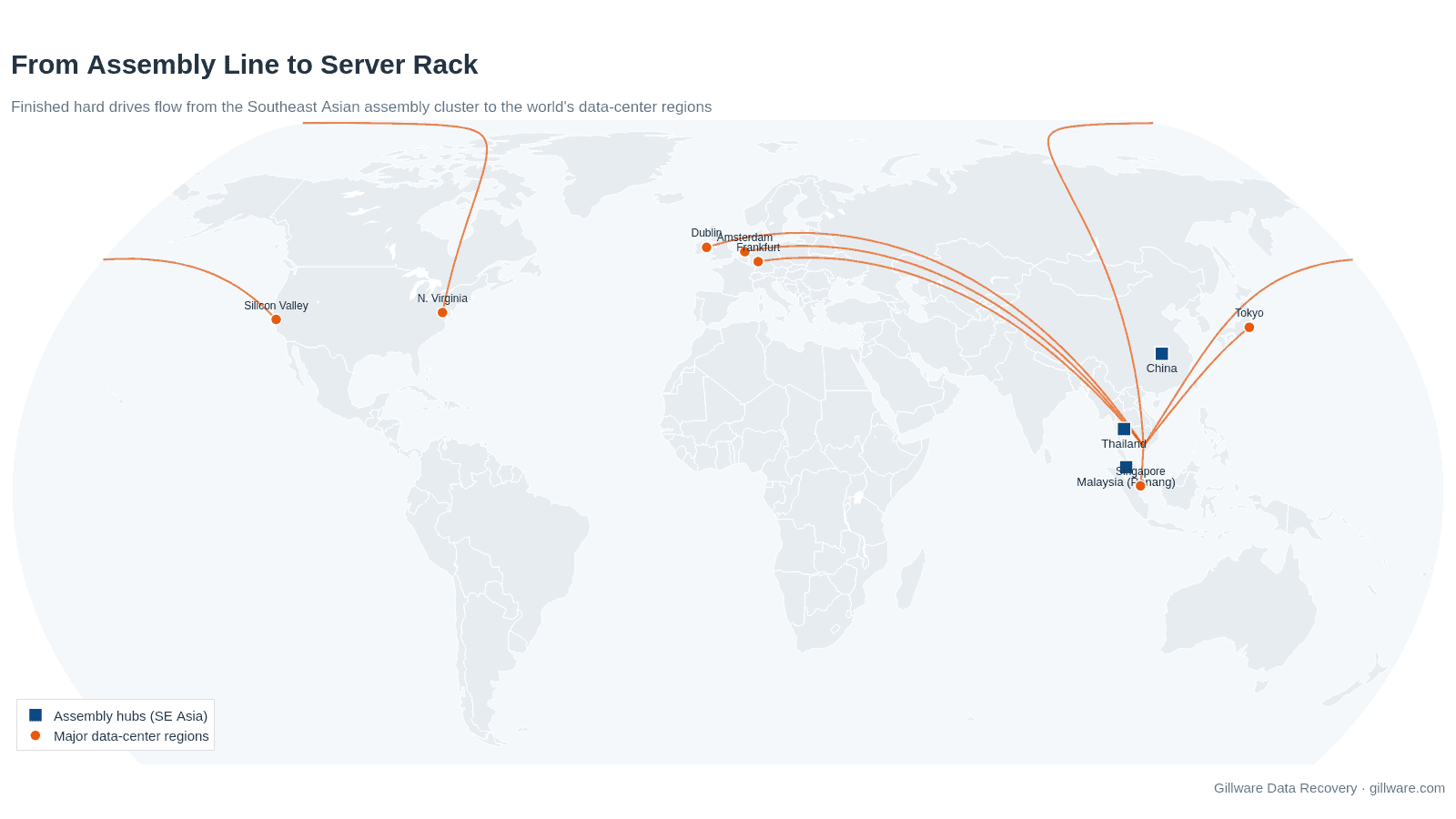

There are only three hard-drive makers left on Earth — Seagate, headquartered in Ireland with major operations in California; Western Digital, based in California; and Toshiba, based in Japan. But “making” a hard drive is really the act of assembling components from a global network of specialists. The map below shows the main manufacturing hubs; the sections that follow walk through each component in turn.

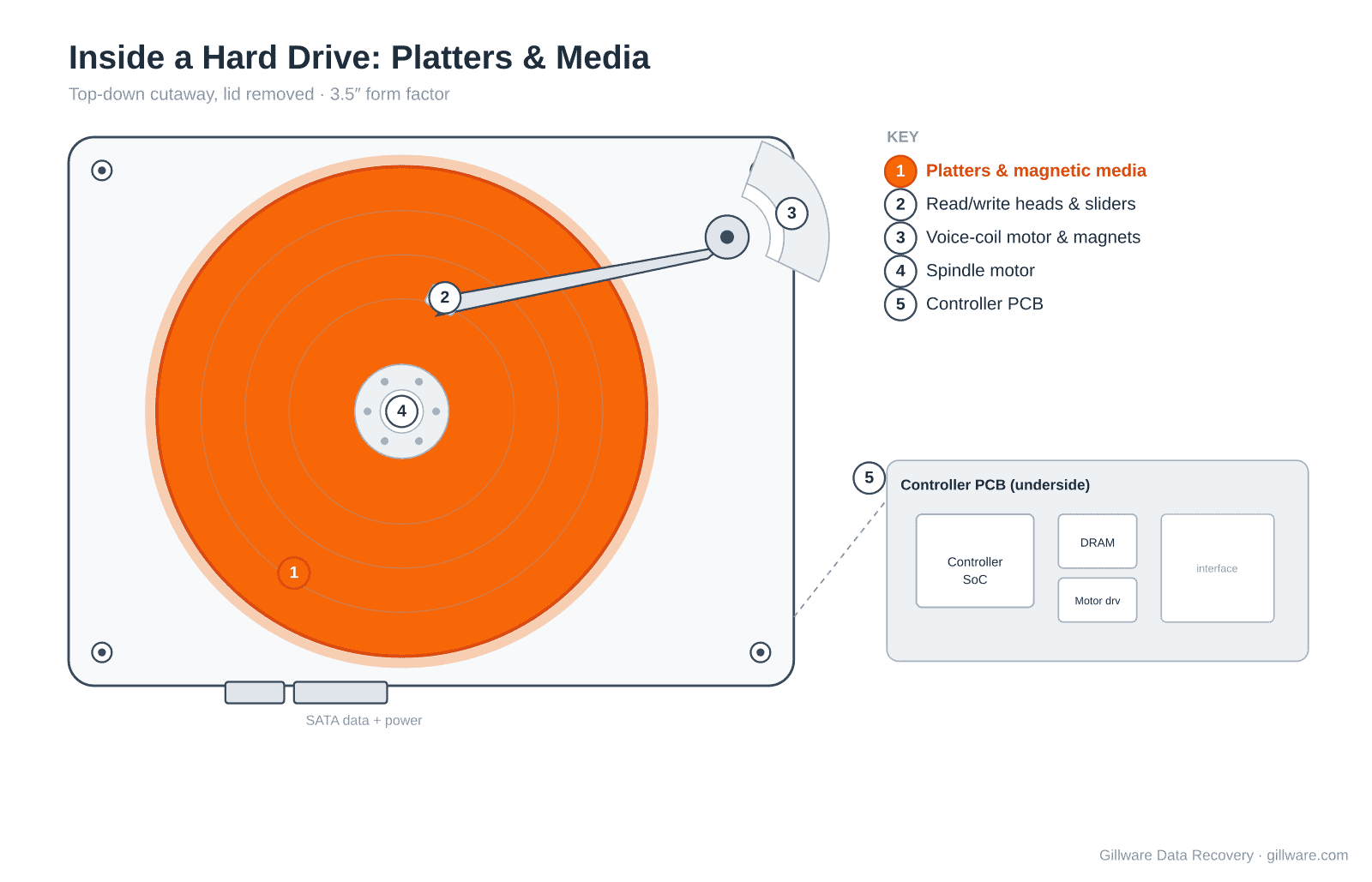

Platters and magnetic media

The platter is where your data physically lives, and it is a marvel of materials engineering. It starts as a substrate — historically an aluminum alloy, but increasingly glass or a glass-ceramic composite, because glass can be polished thinner and flatter and holds its shape better under heat. That matters more every year, because packing more terabytes onto a disk means flying the head closer to a smoother surface. Glass substrates come from a small number of specialist manufacturers, led by Japan’s Hoya, whose disks rank among the smoothest mass-produced surfaces on the planet.

The magic happens in how the magnetic layer is applied. The recording film isn’t painted or plated on — it is grown atom by atom inside a vacuum by magnetron sputtering, a physical vapor deposition process in which energized argon ions blast atoms off a target so they condense onto the spinning disk. A finished platter is really a stack of ultra-thin films laid down in sequence: an adhesion and seed layer, a ruthenium-based interlayer that sets the crystal structure, the granular cobalt-platinum (CoPt) alloy that actually stores the bits, and finally a diamond-like carbon overcoat just a few nanometers thick to protect it all. The whole stack is thinner than a wavelength of light, and every layer has to be uniform across the entire disk.

That deposition step runs on some of the most specialized equipment in the industry, and it too is concentrated. The dominant tool is the 200 Lean sputtering system from Intevac, a California company whose machines have processed roughly 60% of all magnetic disk media produced worldwide. The main alternative comes from Japan’s Canon ANELVA, which supplies physical-vapor-deposition equipment for both magnetic media and read-head manufacturing. HAMR media raises the bar further: its iron-platinum (FePt) recording layer has to be deposited at very high temperatures, which is one reason the transition to higher-capacity drives is as much an equipment story as a materials one. After deposition, the disk gets a molecule-thin layer of PFPE lubricant applied by a precise dip process — the final buffer that lets a head fly nanometers away without catastrophe.

Then comes the part few people ever see: finishing and certification, done with heads that look almost exactly like the ones that will later read your data. A burnish head is swept across the freshly coated surface to knock down microscopic high points, or asperities, that would otherwise cause a crash. A glide head then flies at a deliberately low, fixed height to detect any remaining defects — engineers watch for the “glide avalanche,” the height at which the head starts contacting the surface, as a measure of how clean the disk is. Only after a disk passes burnish, glide, and a full read/write certification pass is it cleared to become part of a drive. These test heads are themselves precision sliders (typically an alumina-titanium-carbide ceramic), and the burnish-glide-certify sequence is a big part of why so few facilities in the world can actually finish media to spec.

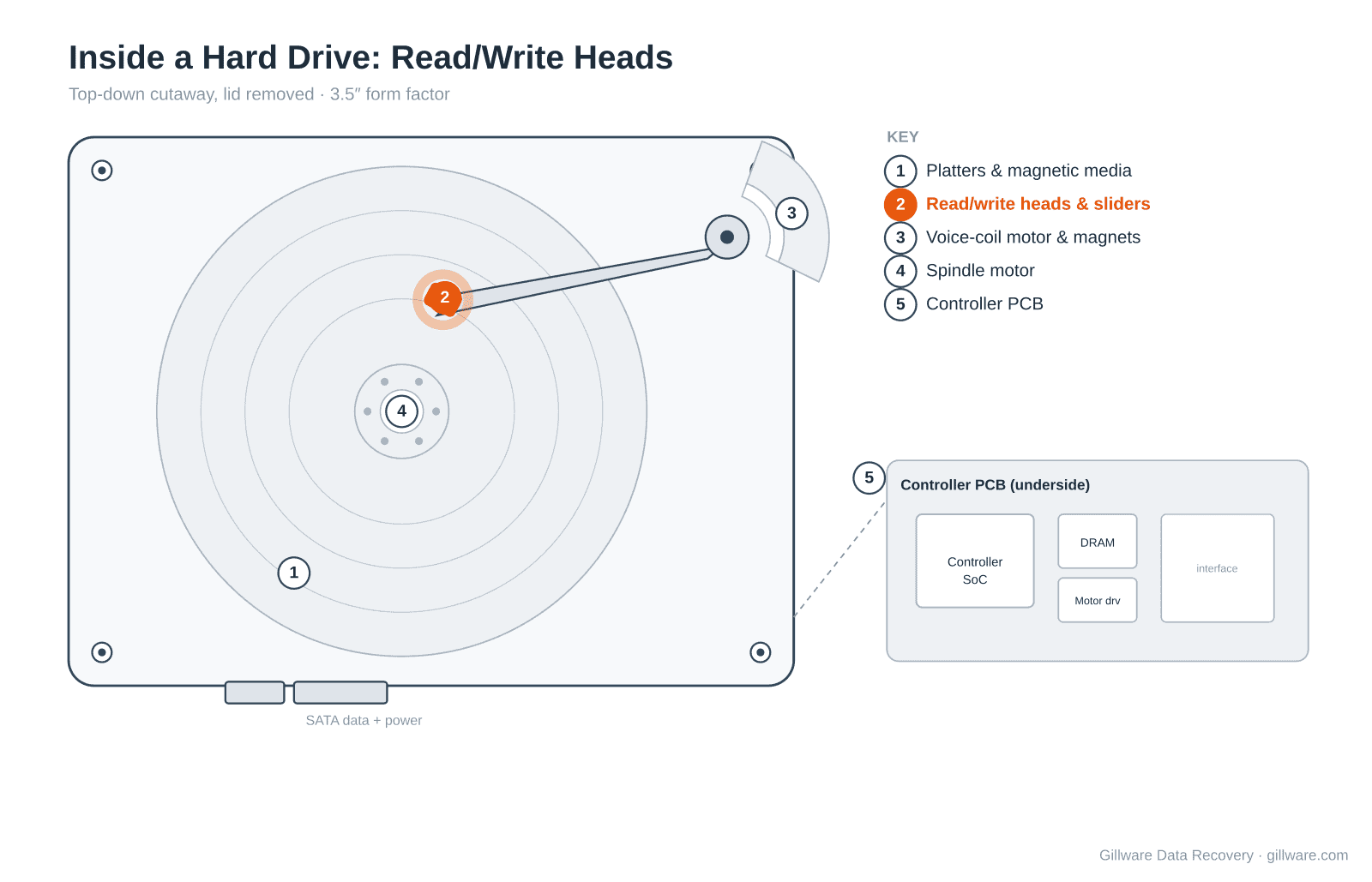

Read/write heads and sliders

If the platter is the page, the read/write head is the pen — and it is arguably the most sophisticated component in the entire drive. A single head is smaller than a grain of dust, built on a wafer using photolithography much like a semiconductor chip. The write head generates a magnetic field precise enough to flip regions of the platter measured in nanometers; the read head is a magnetoresistive sensor whose electrical resistance changes as it passes over those magnetic patterns, so it can tell a one from a zero while flying past at highway speeds.

Head fabrication is one of the most geographically concentrated steps of all. A large share of the world’s read/write heads is made at a single facility: Seagate’s wafer fab in Springtown, near Derry in Northern Ireland, long reported to produce on the order of a third of all HDD heads globally. Seagate and Western Digital run their own head fabs, while Japan’s TDK is the major merchant supplier that historically produced heads for other drive makers. Once the head wafers are fabricated, they are shipped to Southeast Asia — much of it to Thailand — where they are diced into individual sliders and mounted onto the arms to form the head-gimbal and head-stack assemblies. A head, in other words, can be designed in the U.S., etched in Ireland, and assembled in Thailand before it ever meets a platter.

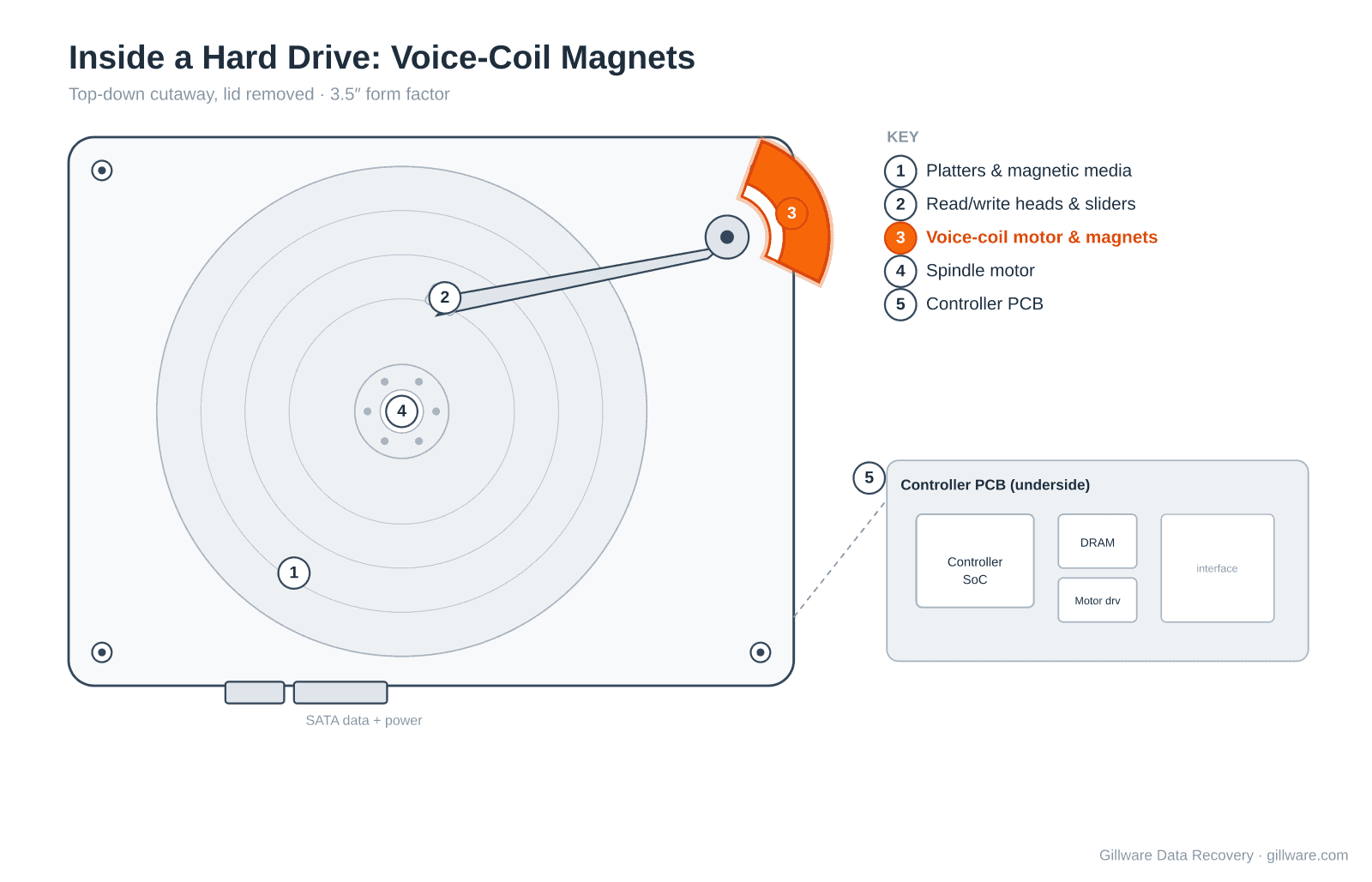

The actuator magnets: hard drives’ rare-earth dependency

To read your files, the drive has to swing its heads to exactly the right track, tens of thousands of times a second, with pinpoint accuracy. That motion comes from the voice-coil motor (VCM): a coil of wire that pushes against a pair of strong permanent magnets. Those magnets are where the hard drive quietly plugs into one of the most contested supply chains on Earth.

The magnets are made of neodymium-iron-boron (NdFeB), the strongest type of permanent magnet in commercial use. To keep their strength at the temperatures inside a running drive, high-performance NdFeB magnets are doped with small amounts of the “heavy” rare-earth elements dysprosium and terbium, which raise the magnet’s resistance to demagnetization. Neodymium, dysprosium, terbium, and their cousins are the rare earths — seventeen chemically similar metals that are not actually rare in the ground but are difficult, dirty, and expensive to separate into usable form.

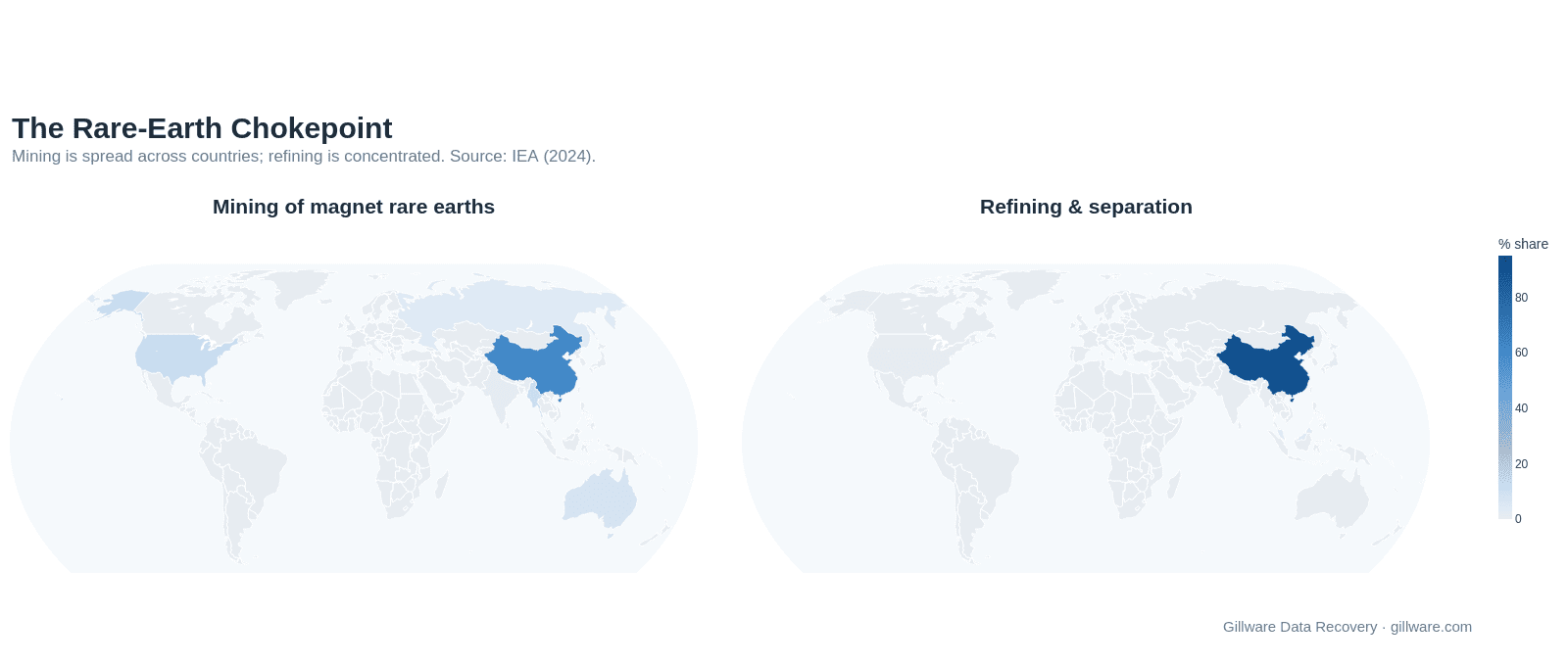

Here the geography narrows dramatically. According to the International Energy Agency, China accounted for roughly 60% of the world’s mined supply of the magnet rare earths in 2024 — and, more strikingly, around 90% of the refining and separation capacity that turns raw ore into magnet-grade material. Other countries mine rare earths — Myanmar, Australia, and the United States among them — but refining and magnet-making capacity outside China remains limited, with Japan one of the few significant producers of finished rare-earth magnets. That means even a magnet made in Japan may depend on refined material that passed through China first.

Because that concentration exists, rare earths have become an instrument of trade policy, and 2025 saw a rapid back-and-forth. In April 2025, China introduced export controls requiring licenses for several heavy rare-earth elements and the magnets that contain them. In October 2025, it announced a broader expansion — adding more elements to the list and, significantly, an extraterritorial rule under which foreign-made magnets could fall under Chinese licensing if they contained as little as 0.1% by value of Chinese-origin rare-earth material. Then, in early November 2025, following diplomatic talks, China suspended the October package and several related measures for roughly a year, into late 2026. In the interim, S&P Global reported that rare-earth prices outside China rose sharply — European prices for some materials reached several times Chinese levels — and that shipments of the most tightly controlled heavy rare earths remained below historical norms.

The upshot is a structural dependency: a critical input to every hard drive sits within a supply chain whose availability can shift with the stroke of a policy pen. The industry has noticed. In 2025 Western Digital launched a program to recover rare-earth materials from retired drives — an acknowledgment that the cheapest new source of neodymium might be the mountain of hard drives the world has already thrown away. (That recycling story is the subject of our next piece.)

A fair question is why the industry doesn’t simply design the rare earths out. The answer is physics and economics. NdFeB magnets offer far more magnetic strength for their size and weight than the rare-earth-free alternatives, and inside a sealed drive with almost no room to spare, that power density is hard to give up without sacrificing performance or capacity. Engineers have made real progress reducing the amount of the most restricted heavy rare earths per magnet, and rare-earth-free magnet chemistries exist for less demanding uses — but for a component that has to move heads with extreme precision billions of times over a drive’s life, wholesale substitution is not a switch anyone can flip quickly. Diversifying the supply — new mines and, crucially, new refining and magnet-making capacity outside the current concentration — is the more realistic path, and analysts broadly agree that building it out at scale is a matter of years, not months.

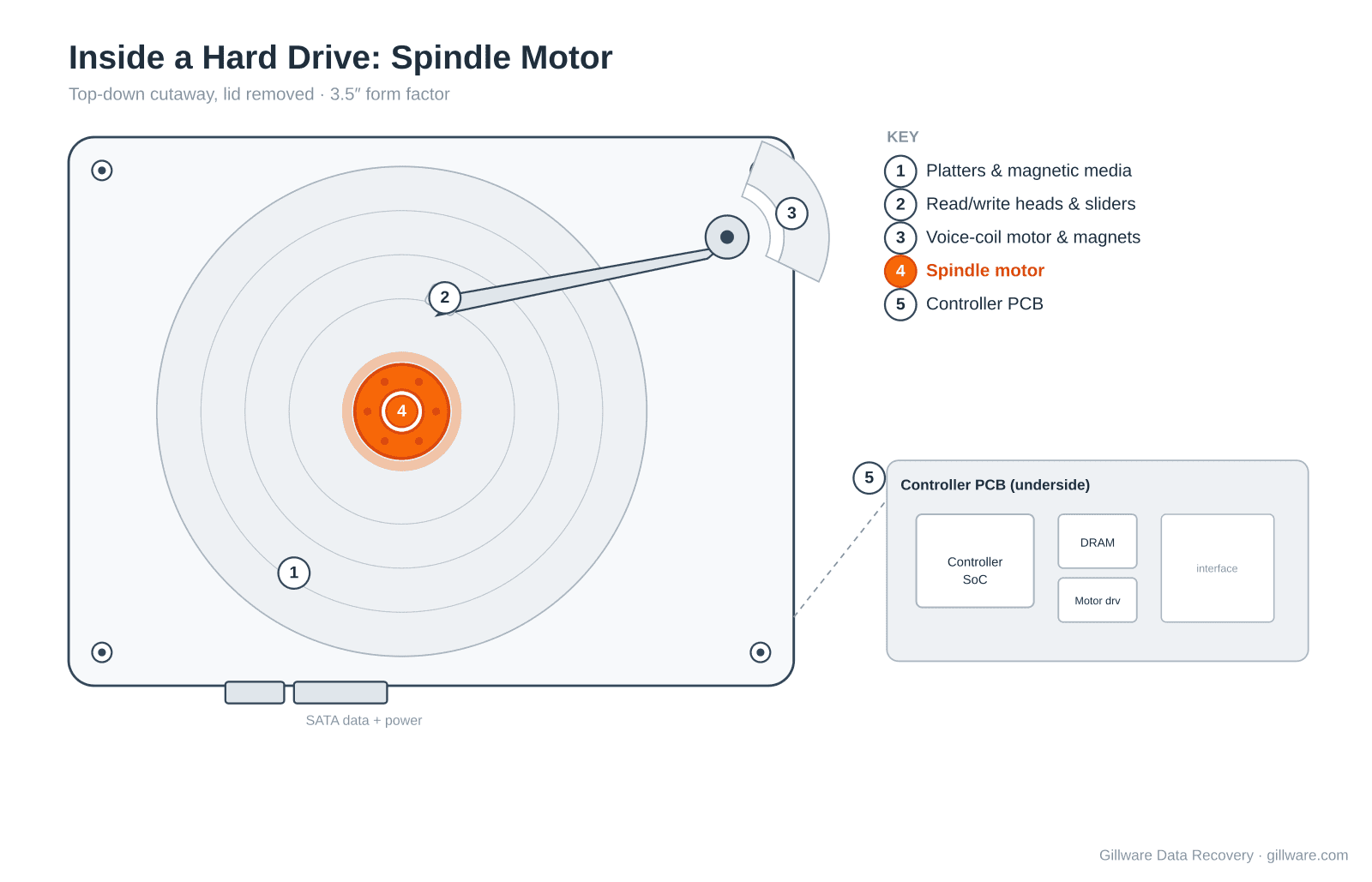

The spindle motor

While the voice-coil motor moves the heads, the spindle motor spins the platters — smoothly, quietly, and at a precisely constant speed for years on end. It sounds mundane, and yet it may be the single most concentrated dependency in the entire drive.

One company, Japan’s Nidec, is estimated to make on the order of 80% of the world’s hard-drive spindle motors, supplying all three of the remaining drive makers. Nidec’s brushless DC motors, increasingly built with fluid-dynamic bearings for stability and quiet running, are the standard the industry is built on. The main alternative supplier is another Japanese firm, MinebeaMitsumi, which makes many of its motor parts in-house and manufactures at a hub in Thailand. When a single supplier makes four out of five of a critical part, its factories become a chokepoint whether anyone intends them to or not — a fact that, as we’ll see, the industry learned the hard way in 2011.

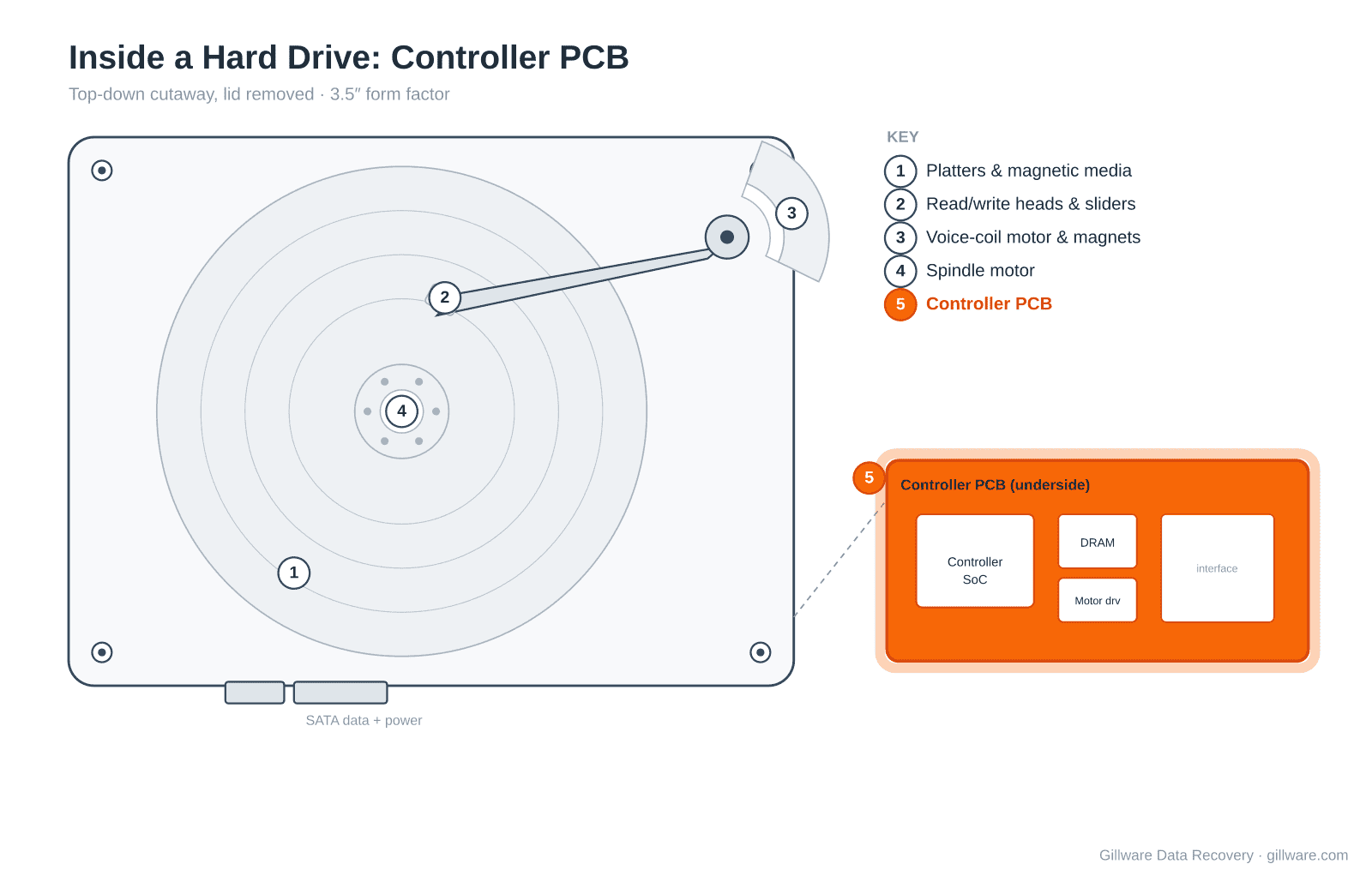

The controller board and the silicon

Bolted to the outside of the sealed drive is the printed circuit board — the drive’s brain. It is worth walking through chip by chip, because this is where a hard drive quietly becomes a semiconductor product, subject to all the pressures of the global chip industry on top of everything else.

The largest chip is the controller system-on-chip (SoC). It integrates several functions that used to be separate chips: the hard-disk controller that talks to the host, an ARM-based processor core, the servo controller that keeps the heads on track, and the read channel — the sophisticated signal-processing engine (using partial-response, maximum-likelihood, or PRML, techniques) that reconstructs clean data from the faint, noisy analog signal coming off the platter. The design of these SoCs is dominated by two names: Seagate’s drives typically run Broadcom silicon, while Western Digital and Toshiba lean on Marvell’s HDD controllers and preamplifiers; enterprise SAS platforms often use Broadcom (formerly LSI) parts. Like most chip companies today, these are “fabless” designers — the physical chips are manufactured by contract foundries, with advanced logic nodes concentrated among a small number of players led by Taiwan’s TSMC. After the wafers are fabricated, they are shipped to outsourced assembly-and-test (OSAT) houses — firms such as ASE and Amkor, largely in Taiwan and elsewhere in Asia — where the wafers are diced into individual chips and packaged. The controller alone therefore threads through chip designers in the U.S., foundries in Taiwan, and packaging plants across Asia before it ever reaches the drive.

Around the SoC sit several supporting chips. A DRAM buffer (typically DDR SDRAM) provides working memory and cache; it comes from the same three memory makers — Samsung, SK Hynix, and Micron — whose output is, in 2026, being fought over by the very AI boom driving hard-drive demand in the first place. A small nonvolatile flash chip, usually a serial NOR device, acts as the drive’s boot ROM: it holds the bootstrap loader and a handful of drive-specific parameters (such as the physical head map and fine positioning offsets) needed just to start up. Curiously, most of the firmware does not live on the board at all — it is stored in a reserved “system area” on the platters themselves, which the drive can only reach after the ROM has loaded enough code to spin up and find it. Some drives also add NAND flash as a media cache. These memory and flash parts trace back to their own concentrated supply base — DRAM and NAND from the big memory makers, and NOR flash largely from Taiwanese specialists such as Winbond and Macronix.

Two more chips round out the electronics. A spindle/VCM driver — often a single “combo” power-management chip — supplies the carefully controlled currents that spin the platters and swing the actuator, and it doubles as the circuit that parks the heads safely if power is lost. And a preamplifier, which does not sit on the external board at all but rides on the flexible cable inside the sealed chamber, right next to the heads; it boosts the almost impossibly faint read signal before it can be corrupted by noise on its way to the read channel. Preamps for the latest energy-assisted (HAMR) drives are themselves specialized parts, supplied by the same controller vendors.

There is a subtler point here that matters enormously once a drive fails. Because the boot ROM and the platter system area together hold calibration data unique to each individual unit — the settings for its particular heads, the growing list of sectors retired over its life, and the translation tables mapping logical addresses to physical locations — you cannot reliably revive a drive with a dead board by bolting on a board from an identical model. The replacement doesn’t know the first drive’s calibration. A modern hard drive behaves as a tightly integrated system of mechanics and firmware, not a box of interchangeable parts.

Final assembly and the journey to the data center

With platters, heads, magnets, motor, and board in hand, the drive is finally assembled — and this, too, happens in a tight cluster of locations. Final assembly is concentrated in Southeast Asia, above all in Thailand, with additional capacity in Malaysia (Western Digital has long run a plant in Penang) and China. Assembly is precision work done in cleanrooms far cleaner than a hospital operating room, because a single speck of dust between a head and a platter spinning at thousands of RPM can destroy the drive. The platter stack is mounted on the spindle, the head-stack assembly is installed, high-capacity drives are filled with helium and hermetically sealed, and the controller board is attached and the firmware written.

Then comes testing. Every enterprise drive is exercised for hours or days to weed out early failures before it is boxed. From the assembly hubs, finished drives move by air and sea to distribution centers and system integrators, and finally into the servers and storage arrays of data centers on every continent. The map below traces that flow from the Southeast Asian assembly cluster to the major data-center markets of North America, Europe, and East Asia.

It is worth pausing on how compressed this whole picture is. Three drive makers. One dominant spindle-motor supplier. A single fab producing a large share of the world’s heads. One country refining most of the rare earths in the magnets. Two vendors designing nearly all the controller silicon. A final-assembly base clustered in a few Southeast Asian provinces. A hard drive looks like a commodity, but it rests on a small set of specialized nodes — and history offers a vivid lesson in what happens when one of those nodes goes offline.

When the chain broke: the 2011 Thailand floods

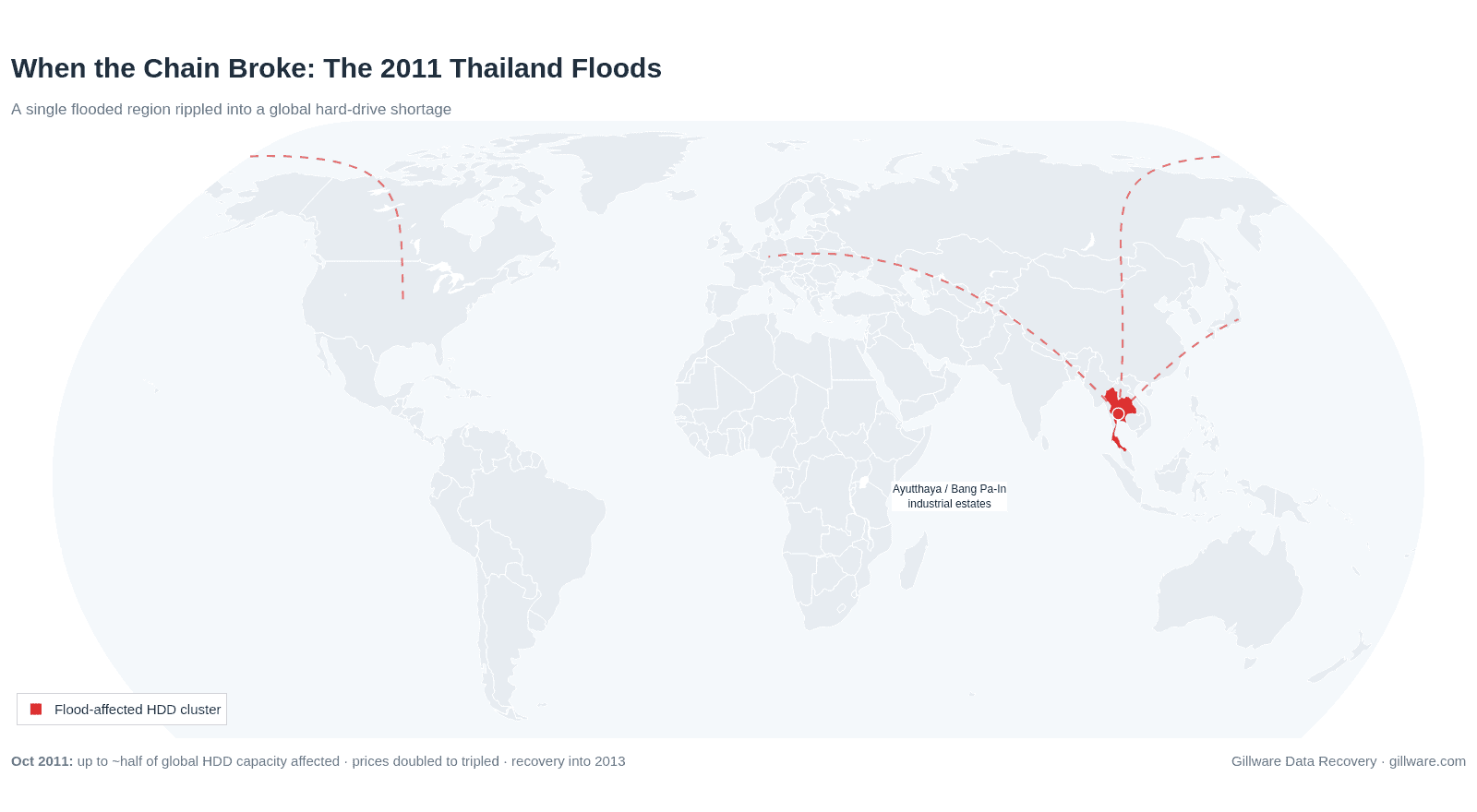

In the second half of 2011, an unusually heavy monsoon season overwhelmed Thailand’s Chao Phraya river basin. By October, floodwaters had inundated the central industrial estates north of Bangkok — including Ayutthaya and Bang Pa-In, home to a dense cluster of hard-drive and component factories. The human cost was severe: more than 800 people died and vast areas were left underwater for weeks. It remains one of the costliest natural disasters in modern history, and its economic aftershocks reached far beyond Thailand’s borders.

Thailand at the time produced a large share of the world’s hard drives — estimates ranged from about a quarter to nearly half of global output, depending on how components were counted. When the factories flooded, the effect was immediate and global. Industry analysts estimated that up to half of the world’s HDD manufacturing capacity was lost or damaged. Prices roughly doubled, and in some retail channels tripled almost overnight. PC makers, chip companies, and storage vendors all felt it: several major system builders and array vendors raised drive prices by double-digit percentages, and one large chipmaker cut its quarterly revenue outlook by around a billion dollars, citing the drive shortage.

What made the episode so instructive was the way the damage rippled through the network we’ve just mapped. Western Digital and Toshiba had factories directly in the flood zone. Seagate’s own plants were largely spared — but Seagate still felt the squeeze, because component partners, including the dominant spindle-motor supplier, had production halted by the water. A single geographic cluster turned out to sit under multiple links of the chain at once.

The recovery was faster than many feared. As IEEE Spectrum documented, Western Digital had its first post-flood drive off the line in about 46 days and returned to normal capacity within months, at a cost the company put in the hundreds of millions of dollars. But the effects lingered. Full industry recovery stretched into 2013. Drive prices never fell all the way back to pre-flood levels; manufacturers’ gross margins actually improved afterward, and some shortened their warranty periods during the crunch. Manufacturers also diversified a little — Western Digital expanded assembly in Malaysia — but the industry did not abandon the Thailand cluster, judging its advantages in labor, infrastructure, and co-located suppliers too valuable to give up. Fifteen years later, that cluster is still central, and the concentration that amplified the 2011 shock is largely still in place.

The 2026 pressure points

Which brings us back to where we started. In 2026, the hard-drive supply chain is under a set of pressures worth laying out plainly, one at a time.

The AI demand shock. The largest force is simple demand. Training and serving modern AI models means storing staggering quantities of data — training sets, model checkpoints, logs, and the images and video that feed and flow out of these systems. Flash storage is too expensive for bulk archives at that scale, so hyperscalers have turned to high-capacity nearline hard drives and bought them in enormous volume. Both major U.S. drive makers told investors in early 2026 that their nearline output was effectively sold out for the year, with capacity committed under long-term agreements stretching toward 2027 and 2028. Industry analyst Tom Coughlin projects total HDD capacity shipped rising from roughly 1.2 zettabytes in 2024 to more than 7 zettabytes by 2029, with the vast majority in high-capacity nearline drives. As Data Center Dynamics reported, lead times for enterprise HDDs have stretched dramatically, and manufacturers are meeting demand mainly by increasing the capacity of each drive — pushing HAMR and other density technologies toward 100-terabyte drives later this decade — rather than building large amounts of new factory capacity.

Rare-earth export controls. Layered on top of surging demand is the materials picture described earlier. The 2025 sequence of export controls, the extraterritorial licensing rule, and the subsequent suspension into late 2026 all point to the same underlying reality: a critical input sits behind a licensing regime that can tighten or loosen with policy. Even when material keeps flowing, prices and lead times for the most tightly controlled heavy rare earths have been volatile, and legal advisers have urged buyers to treat the current pause as temporary and map their exposure accordingly.

Tariffs and trade friction. Beyond rare earths, the broader environment of tariffs and shifting trade rules adds cost and uncertainty to a product whose components cross many borders before final assembly. Each border a component crosses is a place where a duty, a rule change, or a customs delay can add cost or time. For a device assembled from parts sourced across a dozen countries, those frictions accumulate.

Concentration itself. Finally, there is the structural fragility we’ve traced throughout: a handful of drive makers, one dominant spindle-motor supplier, a few head fabs, one country refining most of the magnet rare earths, two controller-silicon designers, and a compact assembly cluster. None of this is a problem on a normal day. It becomes a problem precisely when something abnormal happens to one node — as 2011 demonstrated.

Where it could go from here

What follows is scenario thinking rather than prediction — a few plausible ways the chain could be tested, and what they might mean for the large data-center projects now depending on it. None of these is a forecast that any specific event will occur.

A magnet squeeze. If heavy-rare-earth licensing were to tighten again after the current suspension, magnet lead times could lengthen even if outright shortages never materialize. Drive makers hold inventory and qualify multiple magnet sources, so the near-term effect would more likely show up as cost and scheduling pressure than as empty shelves — but in an already sold-out market, even modest friction has an outsized effect on who gets drives and when.

Another single-node disruption. The 2011 floods are the template: a natural disaster, a fire, or a prolonged outage at a concentrated node — a major head fab, the dominant spindle-motor maker, a media-sputtering line, or the Southeast Asian assembly cluster — could remove a large slice of global capacity quickly. With the industry already running flat out for AI customers, there is little slack to absorb such a shock, which is exactly the condition that turns a regional event into a global price spike.

What it means for data-center projects. For the organizations building large AI and cloud facilities, the practical consequences are about time and priority more than absolute availability. Long lead times mean storage has to be planned and ordered far earlier in a project than it used to be. Allocation increasingly favors the largest buyers with long-term agreements, which can leave smaller operators and traditional enterprise IT waiting. And persistent HDD tightness accelerates a longer-term shift some operators are already making toward all-flash architectures for certain tiers — though flash has its own AI-driven supply constraints, so it is not a simple escape hatch. The reasonable posture, most analysts suggest, is to treat high-capacity storage as a long-lead, strategically sourced input rather than a commodity bought on demand.

The bigger picture

Trace a hard drive all the way back and you end up somewhere unexpected: at a mine, a refinery, a glass polisher, a cleanroom fab, a sputtering line, a chip foundry, a packaging house, and a flood-prone industrial estate — tied together across a dozen countries into a single spinning object. The device is a near-perfect miniature of the modern global economy: enormously capable, astonishingly cheap per terabyte, and quietly dependent on a short list of specialized suppliers that most of the people relying on it have never heard of.

For the investors funding data centers, the policymakers weighing critical-minerals strategy, and the operators planning capacity, that is the takeaway worth holding onto. The hard drive is no longer just a storage device; it is a strategic input whose supply is shaped as much by geology and geopolitics as by engineering. Understanding the chain that produces it — and the handful of points where it narrows — is now part of understanding the infrastructure of artificial intelligence itself.

Coming next in this series

Where hard drives go to die: disposal, e-waste, and the state of HDD recycling in 2026

We followed the hard drive from the mine to the data center. Next, we follow it out the other end — how drives are really disposed of, the environmental footprint of storage at data-center scale, and the growing push to reclaim rare earths and other materials from retired drives, with a timeline of HDD recycling efforts.

Sources and further reading

- International Energy Agency — critical-mineral export controls and rare-earth supply concentration.

- S&P Global Commodity Insights — rare-earth supply bottlenecks and 2026 pricing outlook.

- China Briefing and Clark Hill — China’s 2025 rare-earth export-control announcements and their November 2025 suspension.

- Tom’s Hardware — rare-earth controls and their effect on storage components.

- The Register and Data Center Dynamics — 2026 HDD allocation, lead times, and manufacturer commentary.

- Intevac and Canon ANELVA — magnetic-media sputtering and thin-film deposition equipment.

- Marvell — HDD controller SoCs and preamplifiers.

- Horizon Technology — spindle-motor and platter/media supplier overviews.

- IEEE Spectrum and Backblaze — retrospectives on the 2011 Thailand floods and their impact on global hard-drive supply.

Figures and industry estimates cited above are drawn from the public sources linked here and reflect reporting available at the time of writing in 2026. Conditions in this sector change quickly.

Published by Gillware Data Recovery, a professional data recovery laboratory in Madison, Wisconsin.